marp: true author: Vivaldo Mendes paginate: true math: true style: | .columns { display: grid; grid-template-columns: minmax(0, 50fr) minmax(0, 50fr); } h2 { position: absolute; top: 50px; left: 75px; right: 75px; color: #34429a; font-size: 46px; }

h1 { font-size: 60px } .red { color: #e53935; } .blue { color: #1e88e5; } .cyan { color: #00bcd4; } .purple { color: #8e24aa; } .teal { color: #00897b; } .orange { color: #fb8c00; }

The Hodrick-Prescott Filter

Macroeconomics (M8674)

February 2026

Vivaldo Mendes, ISCTE

vivaldo.mendes@iscte-iul.pt

1. Main goal

Main goal of a filter in macroeconomics

In economics, any filter intends to separate a time-series \(y_t\) into a trend \(\tau_t\) and a cyclical component \(\varphi_t\) such that: \[y_t = \tau_t + \varphi_t \tag{1}\]

- The trend is the long-run component of the time series

- The cyclical component is the short-run component of the time series

Therefore, from (1) we get

\[\varphi_t = y_t - \tau_t \tag{2}\]

- The trick is to minimize eq. (2) subject to some given constraint on \(\varphi_t\)

Types of Filters

- There are various approaches to separate the long-run trend from the short-run cyclical component of a time series \(y(t)\) .

- Linear filter

- Linear filter with breaks

- Nonlinear filters

- Nonlinear filters

- Hodrick-Prescott filter (Hodrick & Prescott, 1997)

- Band Pass filter (Baxter & King, 1999)

- Hamilton filter (James Hamilton, 2017)

- … and some others

Don’t trust the internet or chatbots

- If you do not know what you are doing, you will make stupid mistakes

- The internet is full of wrong (or incomplete) information

- Even very respected sources may mislead you:

- Either you know very well what you are doing, or …

2. The Hodrick-Prescott filter (HP)

The HP filter: some intuition

- We have some data: a time series \(y_t\)

- We want to extract a smooth trend \(\tau_t\) from \(y_t\)

- We want the difference between the two \((\varphi_t)\), to be “acceptable” given what we know about booms and recessions: not too large, not too small

- We introduce a parameter (\(\lambda\)) into a minimization problem to achieve that

- The minimization problem with respect to \(\tau_t\) can be written as:

\[\min _{\tau_{t}} \left\{ {\cal{L(\tau)}} =\sum_{t=1}^{n} \underbrace{\left(y_{t}-\tau_{t}\right)^{2}}_{=\varphi_t^2} +\ {\color{blue}\lambda} \sum_{t=2}^{n-1} \underbrace{\left[\left(\tau_{t+1}-\tau_{t}\right)-\left(\tau_{t}-\tau_{t-1}\right)\right]^{2}}_{\text{constraint}}\right\}\]

The HP filter: Special Cases

The value given to parameter \(\lambda\) is a choice of ours:

\[\min _{\tau_{t}} \left\{ {\cal{L(\tau)}} =\sum_{t=1}^{n} \left(y_{t}-\tau_{t}\right)^{2}+\ {\color{blue}\lambda} \sum_{t=2}^{n-1} \left[\left(\tau_{t+1}-\tau_{t}\right)-\left(\tau_{t}-\tau_{t-1}\right)\right]^{2}\right\}\]

- \(\lambda = 0\) \(\Rightarrow\) trivial solution because there are no cycles : \(y_t= \tau_t, \forall t\)

- \(\lambda \rightarrow \infty \Rightarrow\) linear trend leads to huge cycles between \(y_t\) and \(\tau_t\)

- \(\lambda = 1600\) \(\Rightarrow\) duration/amplitude of cycles acceptable for quarterly data

- \(\lambda = 7\) \(\Rightarrow\) duration/amplitude of cycles acceptable for annual data

- There is no “unquestionable” value for \(\lambda\)

The HP Filter: an Example

- Main objective: obtain cycles as % deviations from the trend

- This has an important implication:

- Time series with a trend: apply logs to the data before extracting the trend and the cycles (

lnGDP,lnCPI) - Time series without a clear trend: do not apply logs to the data (

UR)

- Time series with a trend: apply logs to the data before extracting the trend and the cycles (

- Quarterly data:

US_data.csv - A simple example:

- Real GDP (column

GDP) - Consumer Price Index (column

CPI) - Unemployment Rate (column

UR)

- Real GDP (column

Dealing with rows and columns in a matrix

\(~~~~~~~~~~~~\)

Dealing with rows and columns in a dataframe

To select a column:

- Use its header (

GDPin the example) - It is also possible to use its column number (not shown here)

To select rows:

- Use their numbers (1, 2, 3, …)

- Range of numbers (1:4 in the example)

- No number, just the header: all rows are selected

- Use a condition (e.g.

USdata[USdata.CPI .< 0 , :])

Compute the HP trend and cycles: a single variable

\(~~~~~~\)

Compute the HP trend and cycles: an entire data set

\(~~~~~~\)

Business cycles: Inflation and Unemployment

\(~~~~~~~~~~~~~~~~\)The inflation-gap \(~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~\)The unemployment-gap

The output-gap: logs vs levels

\(~~~~~~\) Correctly measured: using logs \(~~~~~~~~~~~~~~~~~~~\)Incorrectly measured: using levels

3. Use filters with care

Three Major Issues

- There is no perfect filter … but the HP seems very good.

- Measuring Potential GDP and Natural Unemployment is difficult:

- Potential GDP is usually associated with the HP-trend in GDP … but not exclusively.

- The Natural Rate of Unemployment is largely associated with the HP-trend in unemployment.

- The HP filter can be misused for policy purposes:

- The James Bullard 2012 case in the USA is a well-known example.

- The HP filter is very useful but should be used with care.

Limitations of the HP Filter

- New data leads to the rewriting of the history of the economy

- The blue lines: data only up to 2008

- The red lines: data up to 2013

| |

|  |

|

Misuses of the HP Filter

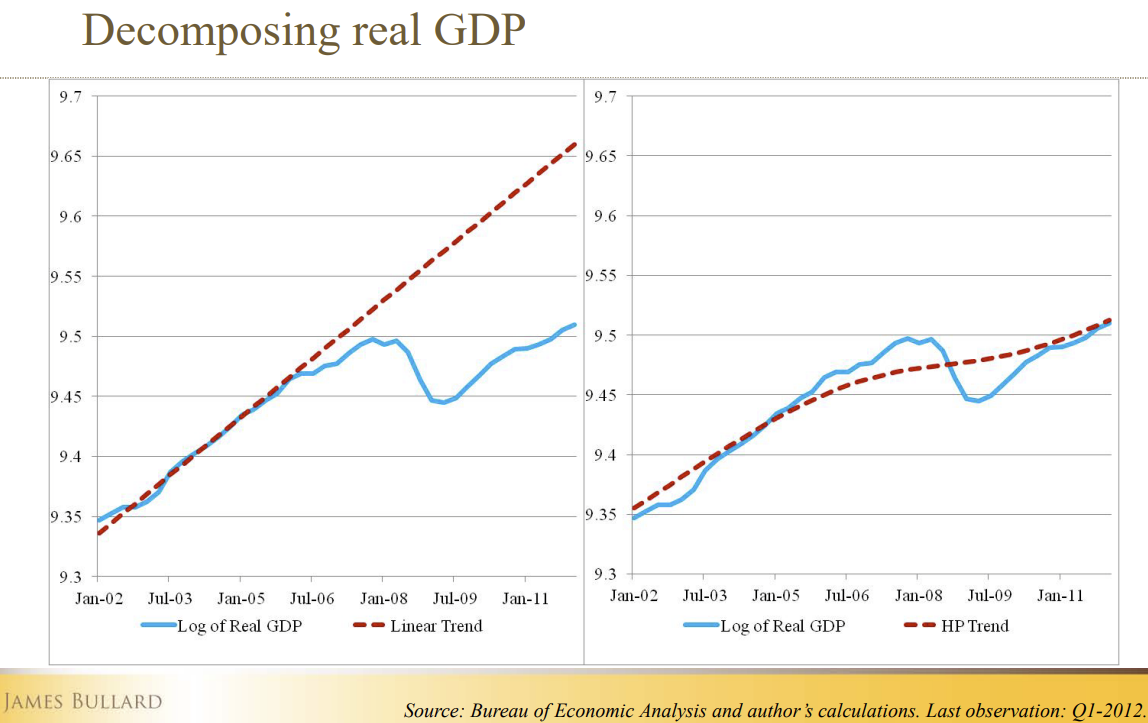

- In 2012, the US economy had an unemployment rate close to 8%, one of the highest rates since WWII.

- The Fed Funds Rate was at 0%, to stimulate the economy.

- The inflation rate was much below the target level (2%) at 0.5% and showing signs of going down.

- James Bullard (the President of the Fed of St. Louis), in a famous speech in June 2012 defended that the US economy had gone back to Potential GDP.

- He strongly pushed for a sharp increase in the Fed Funds Rate.

- He used the HP-filter to substantiate his proposal.

The HP filter according to James Bullard

\(~~~~~~~~\)

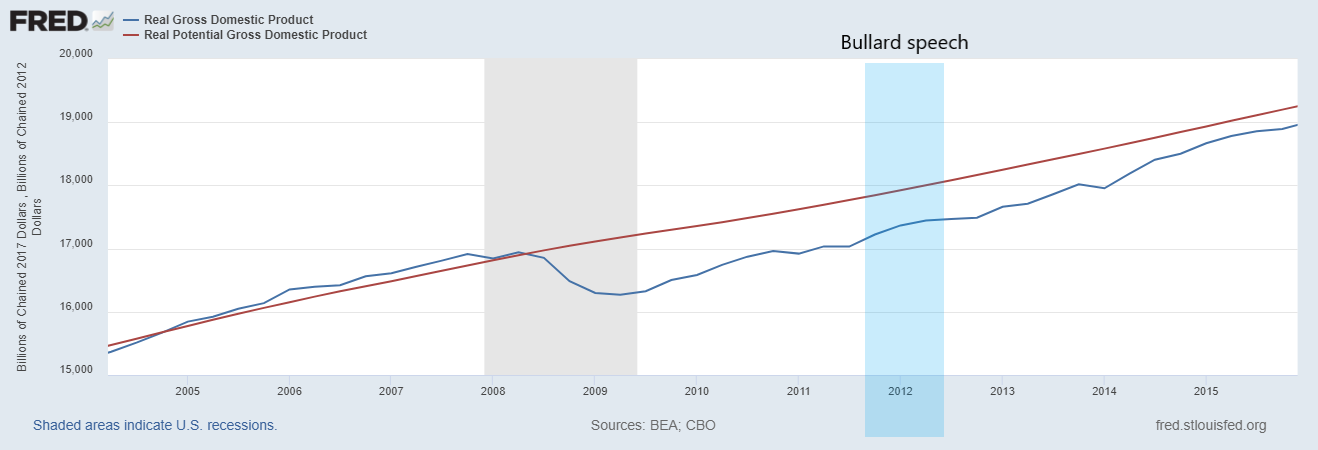

The Output-gap according to the Fed of St. Louis

- The Fed of St. Louis publishes “oficial” US data for Real GDP and Potential GDP.

- Real GDP is the blue line; Potential GDP is the red line.

HP filter & the Natural Unemployment Rate (NUR)

No, Covid-19 did not raise the NUR; no, an increase in NUR did not anticipate Covid-19!

Appendix: HP Filter Derivation

Not compulsory reading

Minimization of the Loss function

The loss function \(\cal{L(\tau)}\) is given by:

\[\mathcal{L}(\tau)=\sum_{t=1}^n\left(y_t-\tau_t\right)^2+ {\color{blue}\lambda} \sum_{t=2}^{n-1}\left[\left(\tau_{t+1}-\tau_t\right)-\left(\tau_t-\tau_{t-1}\right)\right]^2\]

To minimize the Loss function with respect to \(\tau_t\):

\[\min _{\tau_t}\{\mathcal{L}(\tau)\}\]

Take the derivatives with respect to \(\tau_t\) and setting them to zero:

\[\frac{\partial \mathcal{L}(\tau)}{\partial \tau_t} = 0, \quad \forall t=1, \ldots, n\]

Those derivatives are known as the First Order Conditions (FOCs).

First Order Conditions (FOCs)

- For \(\tau_1:\)

- \({ {\cal{L}}(\tau_1)}=(y_1-\tau_1)^2 +\lambda [\tau_3-2 \tau_2 + \tau_1)]^2\)

- \(\frac{\partial {\cal{L}}(\tau_1)}{\partial \tau_1} = -2\left(y_1-\tau_1\right)+2 \lambda\left(\tau_3-2 \tau_2+\tau_1\right)=0\)

- \((1+\lambda) \tau_1-2 \lambda \tau_2+\lambda \tau_3=y_1 \tag{FOC1}\)

- For \(\tau_2:\)

- \({ {\cal{L}}(\tau_2)}=(y_2-\tau_2)^2 +\lambda [\tau_4- 2 \tau_3 + \tau_2)]^2 + \lambda[(\tau_3-2 \tau_2+\tau_1)]^2\)

- \(\frac{\partial {\cal{L}}(\tau_2)}{\partial \tau_2} = -2\left(y_2-\tau_2\right) + 2 \lambda\left[ \left (\tau_4-2 \tau_3+\tau_2\right) -2\left(\tau_3-2 \tau_2+\tau_1\right)\right]=0\)

- \((1+5 \lambda) \tau_2-2 \lambda \tau_1-4 \lambda \tau_3+\lambda \tau_4=y_2 \tag{FOC2}\)

First Order Conditions (FOCs): continuation

For \(\tau_t\), such that \(t=3, \ldots, n-2\), the FOC is given by:

- \(-2\left(y_t-\tau_t\right)+2 \lambda\left(\tau_{t-2}-4 \tau_{t-1}+6 \tau_t-4 \tau_{t+1}+\tau_{t+2}\right)=0\) or

- \((1+6 \lambda) \tau_t-4 \lambda \tau_{t-1}-4 \lambda \tau_{t+1}+\lambda \tau_{t-2}+\lambda \tau_{t+2}=y_t\)

And for the two right boundary conditions \((n-1, n)\), we have the following FOCs (they are symmetric to those on the left boundary)

- \((1+5 \lambda) \tau_{n-1}-2 \lambda \tau_n-4 \lambda \tau_{n-2}+\lambda \tau_{n-3}=y_{n-1} \tag{FOCn-1}\)

- \((1+\lambda) \tau_n-2 \lambda \tau_{n-1}+\lambda \tau_{n-2}=y_n \tag{FOCn}\)

First Order Conditions (FOCs): Matrix form

The 5 FOCS that represent the optimal conditions on the left boundary, the right boundary, and the interior conditions \((3 \leq t \leq n-2)\) are:

\[

\begin{aligned}

& (1+\lambda) \tau_1-2 \lambda \tau_2+\lambda \tau_3=y_1 \\

& (1+5 \lambda) \tau_2-2 \lambda \tau_1-4 \lambda \tau_3+\lambda \tau_4=y_2 \\

& (1+6 \lambda) \tau_t-4 \lambda\left(\tau_{t-1}+\tau_{t+1}\right)+\lambda\left(\tau_{t-2}+\tau_{t+2}\right)=y_t, \quad 3 \leq t \leq n-2 \\

& (1+5 \lambda) \tau_{n-1}-2 \lambda \tau_n-4 \lambda \tau_{n-2}+\lambda \tau_{n-3}=y_{n-1} \\

& (1+\lambda) \tau_n-2 \lambda \tau_{n-1}+\lambda \tau_{n-2}=y_n

\end{aligned}

\]

So, we can write:

\[A(\lambda) \tau=y\]

An example with n=6

- \(t=1\)

\(\mathcal{L}(\tau_1)=\left(y_1-\tau_1\right)^2+\lambda\left(\tau_3-2 \tau_2+\tau_1\right)^2\)

\(\frac{\partial \mathcal{L}}{\partial \tau_1}=-2\left(y_1-\tau_1\right)+2 \lambda\left(\tau_3-2 \tau_2+\tau_1\right)=0\)

\((1+\lambda) \tau_1-2 \lambda \tau_2+\lambda \tau_3=y_1\)

- \(t=2\)

\(\mathcal{L}(\tau_2)=\left(y_2-\tau_2\right)^2+\lambda\left(\tau_4-2 \tau_3+\tau_2\right)^2+\lambda\left(\tau_3-2 \tau_2+\tau_1\right)^2\)

\(\frac{\partial \mathcal{L}}{\partial \tau_2}=-2\left(y_2-\tau_2\right) + 2\lambda [\left(\tau_4- 2 \tau_3+\tau_2\right) - 2 \left(\tau_3-2 \tau_2+\tau_1\right)] =0\)

\((1+5 \lambda) \tau_2-2 \lambda \tau_1-4 \lambda \tau_3+\lambda \tau_4=y_2\)

An example with n=6 (cont.)

- \(t=3\)

\(\mathcal{L}(\tau_3)=\left(y_3-\tau_3\right)^2 +\lambda\left(\tau_5-2 \tau_4+\tau_3\right)^2 +\lambda\left(\tau_4-2 \tau_3+\tau_2\right)^2 +\lambda\left(\tau_3-2 \tau_2+\tau_1\right)^2\)

\(\frac{\partial \mathcal{L}}{\partial \tau_3}=-2\left(y_3-\tau_3\right)+2 \lambda\left[\left(\tau_5-2 \tau_4+\tau_3\right) -2\left(\tau_4-2 \tau_3+\tau_2\right)+ \left(\tau_3-2 \tau_2+\tau_1\right)\right]\)

\((1+6 \lambda) \tau_3-4 \lambda \tau_2-4 \lambda \tau_4+\lambda \tau_1+\lambda \tau_5=y_3\)

- \(t=4\)

\(\begin{array}{r}\mathcal{L}\left(\tau_4\right)=\left(y_4-\tau_4\right)^2+\lambda\left(\tau_6-2 \tau_5+\tau_4\right)^2+\lambda\left(\tau_5-2 \tau_4+\tau_3\right)^2+\lambda\left(\tau_4-2 \tau_3+\tau_2\right)^2+ \\ \lambda\left(\tau_3-2 \tau_2+\tau_1\right)^2\end{array}\)

\(\frac{\partial \mathcal{L}}{\partial \tau_4}=-2\left(y_4-\tau_4\right)= 2\lambda [\left(\tau_6-2 \tau_5+\tau_4\right) -2\left(\tau_5-2 \tau_4+\tau_3\right)+ \left(\tau_4-2 \tau_3+\tau_2\right)]=0\)

\((1+6 \lambda) \tau_4-4 \lambda \tau_3-4 \lambda \tau_5+\lambda \tau_2+\lambda \tau_6=y_4\)

An example with n=6 (cont.)

- \(t=5\)

\(\mathcal{L}(\tau_5)=\left(y_5-\tau_5\right)^2 +\lambda\left({\color{blue}\tau_7}-2 \tau_6+\tau_5\right)^2 +\lambda\left(\tau_6-2 \tau_5+\tau_4\right)^2 + ...\)

- This is not a viable way to writing down the Lagrangian function to minimize the problem because \(\tau_7\) is not an interior index, as we have only 6 observations.

- We have to apply the boundary condition that the number of observations end at \(t=6.\)

- Then we will move backward to \(t=5\).

- When we get the results for \(\tau_6\) and \(\tau_5\), the entire solution set is known.

An example with n=6 (cont.)

At the initial boundary we iterate forward, at the end boundary we iterate backwards

- \(t=6\)

\(\mathcal{L}(\tau_6)=\left(y_6-\tau_6\right)^2+\lambda\left(\tau_6-2 \tau_5+\tau_4\right)^2\)

\(\frac{\partial \mathcal{L}}{\partial \tau_6}=-2\left(y_6-\tau_6\right)+2 \lambda\left(\tau_6-2 \tau_5+\tau_4\right)=0\)

\((1+\lambda) \tau_6-2 \lambda \tau_5+\lambda \tau_4=y_6\)

- \(t=5\)

\(\mathcal{L}(\tau_5)=\left(y_5-\tau_5\right)^2+\lambda\left(\tau_5-2 \tau_4+\tau_3\right)^2+\lambda\left(\tau_6-2 \tau_5+\tau_4\right)^2\)

\(\frac{\partial \mathcal{L}}{\partial \tau_5}=-2\left(y_5-\tau_5\right)+2 \lambda\left[\left(\tau_5 - 2 \tau_4+\tau_3\right) - 2\left(\tau_6 -2 \tau_5+\tau_4\right)\right]\)

\((1+5 \lambda) \tau_5-4 \lambda \tau_4-2 \lambda \tau_6+\lambda \tau_3=y_5\)

An example with n=6: all FOCs

\(t=1 \rightarrow (1+\lambda) \tau_1-2 \lambda \tau_2+\lambda \tau_3=y_1\) \(t=2 \rightarrow (1+5 \lambda) \tau_2-2 \lambda \tau_1-4 \lambda \tau_3+\lambda \tau_4=y_2\) \(t=3 \rightarrow (1+6 \lambda) \tau_3-4 \lambda \tau_2-4 \lambda \tau_4+\lambda \tau_1+\lambda \tau_5=y_3\) \(t=4 \rightarrow (1+6 \lambda) \tau_4-4 \lambda \tau_3-4 \lambda \tau_5+\lambda \tau_2+\lambda \tau_6=y_4\) \(t=5 \rightarrow (1+5 \lambda) \tau_5-4 \lambda \tau_4-2 \lambda \tau_6+\lambda \tau_3=y_5\) \(t=6 \rightarrow (1+\lambda) \tau_6-2 \lambda \tau_5+\lambda \tau_4=y_6\)

An example with n=6

If n = 6, the dense form of A is given by: \[ A=\left[\begin{array}{cccccc} 1+\lambda & -2 \lambda & \lambda & 0 & 0 & 0 \\ -2 \lambda & 1+5 \lambda & -4 \lambda & \lambda & 0 & 0 \\ \lambda & -4 \lambda & 1+6 \lambda & -4 \lambda & \lambda & 0 \\ 0 & \lambda & -4 \lambda & 1+6 \lambda & -4 \lambda & \lambda \\ 0 & 0 & \lambda & -4 \lambda & 1+5 \lambda & -2 \lambda \\ 0 & 0 & 0 & \lambda & -2 \lambda & 1+\lambda \end{array}\right] \]

Notice the symmetry of matrix A

- \(diag_2 = [λ, λ, λ, λ]\).

- \(diag_1 = [-2λ, -4λ, -4λ, -4λ, -2λ]\),

- \(diag_0 = [1+λ, 1+5λ, 1+6λ, 1+6λ, 1+5λ, 1+λ]\),

Notebook implementation

- Matrix A non-trivial diagonals:

- \(diag_2 = [λ, λ, λ, λ]\).

- \(diag_1 = [-2λ, -4λ, -4λ, -4λ, -2λ]\),

- \(diag_0 = [1+λ, 1+5λ, 1+6λ, 1+6λ, 1+5λ, 1+λ]\),

- \(diag_{-1} = [-2λ, -4λ, -4λ, -4λ, -2λ]\),

- \(diag_{-2} = [λ, λ, λ, λ]\).

- Check the function

hp_trendin the notebookHP_IRF_2026.jl

4. Readings

Point 2

For this point, there is no compulsory reading.

However, Dirk Krueger (2007). “Quantitative Macroeconomics: An Introduction” (Chapter 2), manuscript, Department of Economics University of Pennsylvania, is well suited for the material covered here.

This text is a small one (12 pages), easy to read, and beneficial for studying the stylized facts of business cycles, mainly to understand how the Hodrick-Prescott filter is calculated. However, notice that, as mentioned, it is not compulsory reading.

Point 3

- No textbook covers the topics/controversies mentioned in this section.

- This coursework intends to provide a framework for a better understanding of these controversies at the end of the course.

- All we have to handle is:

- A little bit of mathematics

- A little bit of computation

- A little bit of macroeconomics